Royal Academy of Engineering: Spotlight on Spinouts 2026

Focus: North East England and Scottish Universities

The UK picture

UK spinout activity is becoming increasingly geographically diverse, with strong growth beyond the Golden Triangle. More than 2,000 spinouts have emerged since 2010, with a combined value of £49 billion and a clear acceleration from 2015 onwards. These companies have created 27,000 jobs, with 70% of those created since 2020.

Scottish universities: strong performers on the European stage

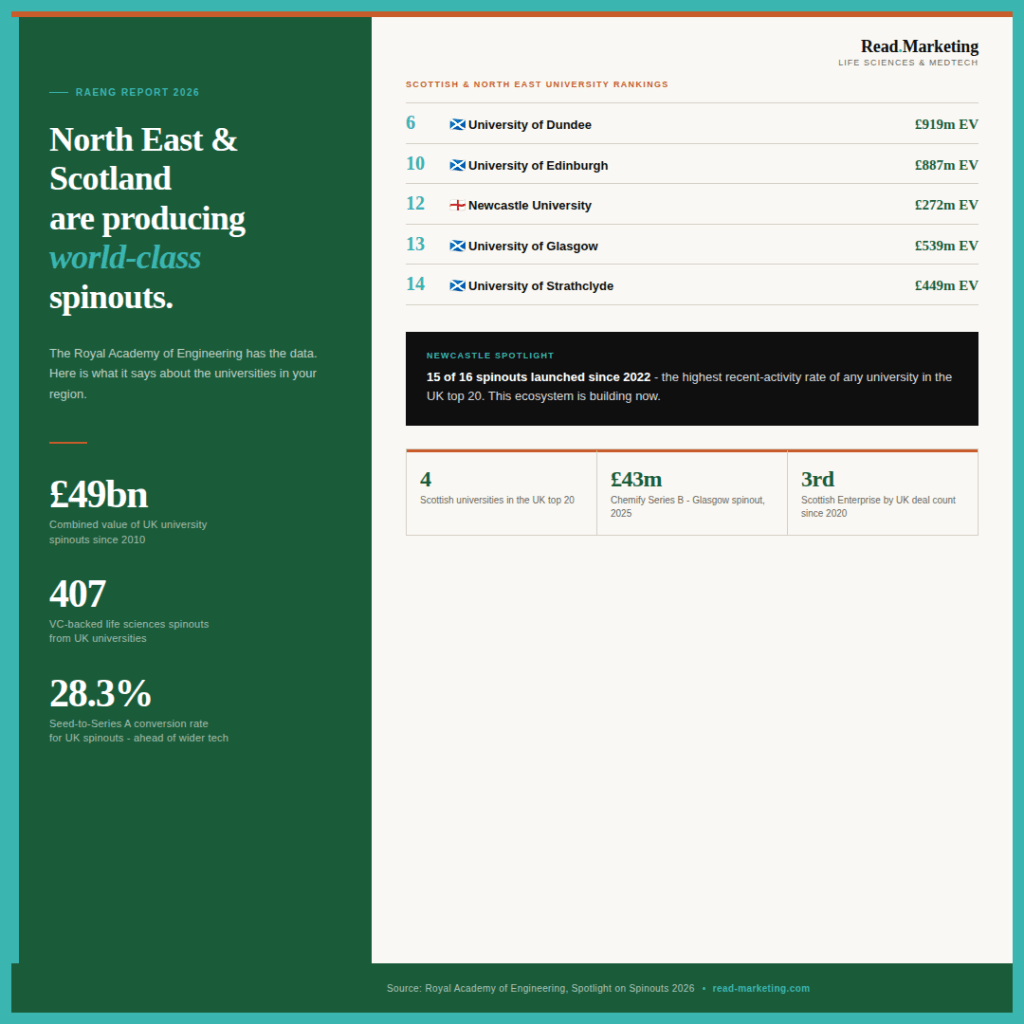

The University of Dundee is the top-ranked university in Scotland, finishing 6th overall in the UK rankings, with 11 VC-backed spinouts, 4 reaching $10m+ in funding, and a combined enterprise value of £919m – largely driven by the success of Exscientia.

The University of Edinburgh ranks 10th in the UK with 28 VC-backed spinouts, 11 reaching $10m+ funding, and £887m in combined enterprise value. The University of Glasgow ranks 13th with 16 VC-backed spinouts and £539m in enterprise value. The University of Strathclyde ranks 14th with 13 VC-backed spinouts and £449m in enterprise value.

Both Edinburgh and Strathclyde feature in the European top 40 for spinout value creation. Chemify, a techbio spinout from the University of Glasgow focused on AI-driven drug synthesis, raised a £43m Series B round in 2025 – one of the top VC deals for UK spinouts that year.

On equity terms, Scottish universities are broadly aligning with best practice: the University of Edinburgh averages a 24% non-cash equity stake (2020-2025) and the University of Strathclyde averages 19% – both in or close to the recommended ranges.

Scottish Enterprise Growth Investments is one of the most active investors in UK spinouts by deal count, participating in 58 rounds since 2020 and 101 since 2015 – placing it third in the UK by activity. That’s direct, accessible public capital for Scottish spin-outs at seed stage.

North East England: a cluster with real momentum

Newcastle University ranks 12th in the UK for spinout value creation, with 16 VC-backed spinouts, 15 of which were launched since 2022 – the highest recent-activity rate of any university in the top 20. Newcastle has generated £272m in combined enterprise value. The high number of recent spinouts is a significant signal: this is a university in active commercialisation mode right now.

Northstar Ventures appears in the top investors list with 25 rounds since 2020, making it one of the most active seed-stage investors in the UK spinout ecosystem. For North East founders, this is domestic capital with regional knowledge.

One area for attention: Newcastle University’s average non-cash equity stake sits at 41% (2020-2025), which is above the recommended range under the Independent Review guidelines. Founders spinning out of Newcastle should understand this context and engage early with the TTO on equity terms.

Life sciences dominates – and that’s the North East and Scotland story

Life sciences is the largest sector for UK spinouts, with 407 VC-backed companies and £26.7bn in combined enterprise value. Biotech and pharma alone accounts for 278 VC-backed spinouts worth over £20.7bn. Medical devices follows with 110 VC-backed spinouts worth £4.2bn.

Spinouts convert from seed to Series A at a rate of 28.3% – marginally ahead of the rest of the UK tech ecosystem at 27.1%, and 21% higher at Series C stage. Life sciences spinouts from UK universities took university equity stakes averaging 20% in 2024-2025, within the recommended range.

What this means for early-stage spin-outs in the region

The data confirms what the best North East and Scottish founders already know: the research base is genuinely world-class and the commercial opportunity is real. The practical priorities coming out of this report are:

- Know your university’s equity position before you start negotiations – it varies significantly and Newcastle in particular warrants close attention.

- Scottish founders have direct access to one of the UK’s most active public investors in Scottish Enterprise Growth Investments. Use it.

- Recent spinout pace at Newcastle suggests a growing ecosystem of peer founders – a network worth building from day one.

- Life sciences conversion rates from seed to Series A outperform the rest of UK tech. The challenge is getting to a well-structured seed round, not surviving beyond it.

Source: Royal Academy of Engineering, Spotlight on Spinouts 2026, powered by Dealroom data.

Ready to build your marketing strategy?

Read Marketing works with biotech, medtech and medical device start-ups across the North East and Scotland to develop marketing strategies that match the stage and ambition of your business.

Leave a comment